When building risk scorecards, apart from the variety of performance metrics, analysts also assess something known as risk-ranking i.e. whether or not the observed event rates increase (or decrease) monotonically with increasing (or decreasing) scores. Sometimes, models are not able to risk-rank borrowers in the tails (regions of very high or very low scores). While this is expected, it would be nice if we could quantify this effect. One way to do this would be to use bootstrapped samples to assess variability in model predictions.

Basic idea

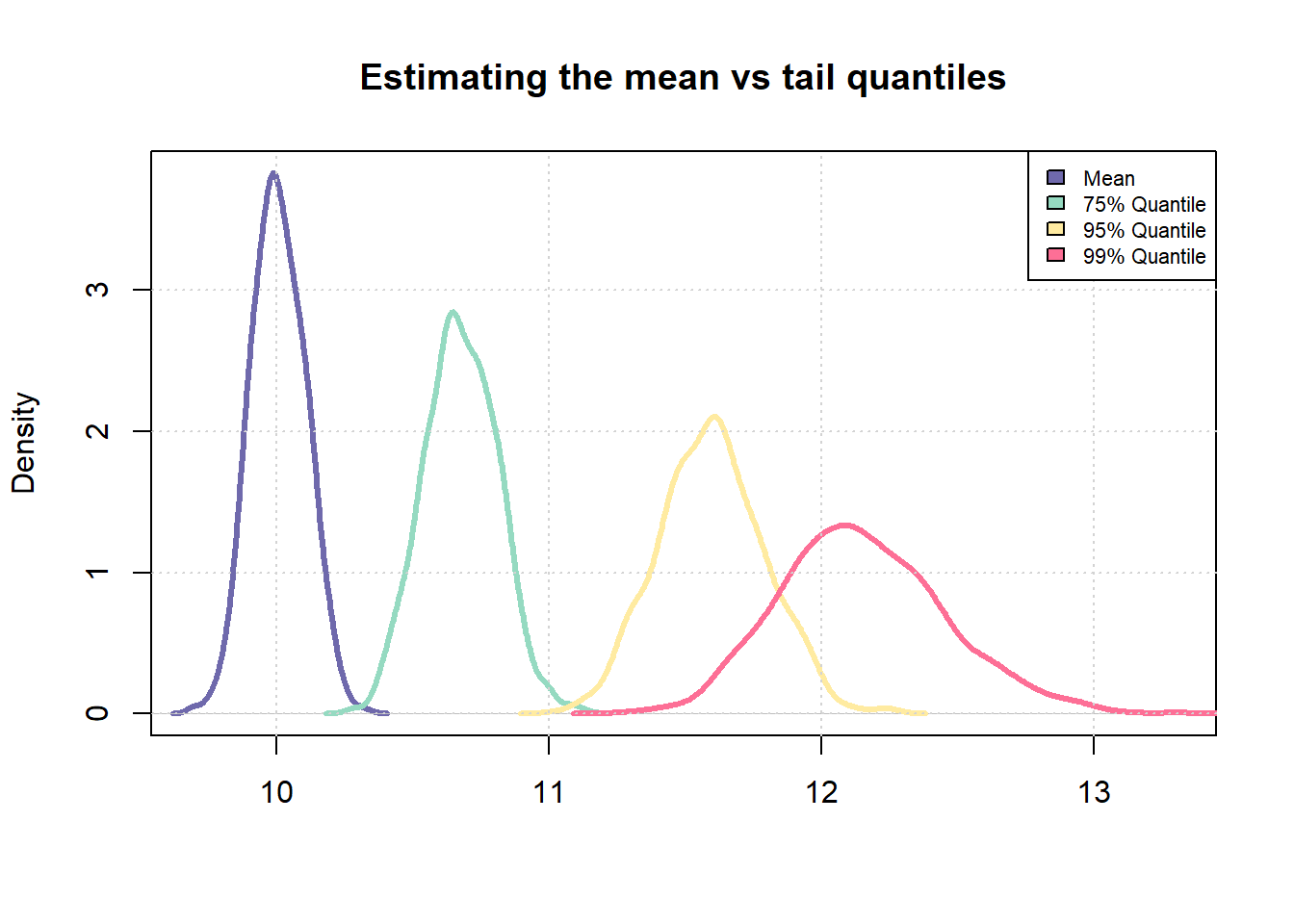

The underlying idea is very simple - less available data for estimation equates to lower quality of estimation. As a simple example, we can observe this effect when trying to estimate quantiles of a probability distribution.

# Number of samples to be drawn from a probability distribution

n_samples <- 1000

# Number of times, sampling should be repeated

repeats <- 100

# Mean and std-dev for a standard normal distribution

mu <- 5

std_dev <- 2

# Sample

samples <- rnorm(n_samples * repeats, mean = 10)

# Fit into a matrix like object with `n_samples' number of rows

# and `repeats` number of columns

samples <- matrix(samples, nrow = n_samples, ncol = repeats)

# Compute mean across each column

sample_means <- apply(samples, 1, mean)

# Similarly, compute 75% and 95% quantile across each column

sample_75_quantile <- apply(samples, 1, quantile, p = 0.75)

sample_95_quantile <- apply(samples, 1, quantile, p = 0.95)

sample_99_quantile <- apply(samples, 1, quantile, p = 0.99)

sd(sample_means)/mean(sample_means)

## [1] 0.01001566

sd(sample_75_quantile)/mean(sample_75_quantile)

## [1] 0.01272449

sd(sample_95_quantile)/mean(sample_75_quantile)

## [1] 0.01822555

combined_vec <- c(sample_means, sample_75_quantile, sample_95_quantile, sample_99_quantile)

plot(density(sample_means),

col = "#6F69AC",

lwd = 3,

main = "Estimating the mean vs tail quantiles",

xlab = "",

xlim = c(min(combined_vec), max(combined_vec)))

lines(density(sample_75_quantile), col = "#95DAC1", lwd = 3)

lines(density(sample_95_quantile), col = "#FFEBA1", lwd = 3)

lines(density(sample_99_quantile), col = "#FD6F96", lwd = 3)

grid()

legend("topright",

fill = c("#6F69AC", "#95DAC1", "#FFEBA1", "#FD6F96"),

legend = c("Mean", "75% Quantile", "95% Quantile", "99% Quantile"),

cex = 0.7)

It is easy to notice that the uncertainty in estimating the sample 99% quantile is much higher than the uncertainty in estimating the sample mean. We will now try to extend this idea to a scorecard model.

Libraries

#install.packages("pacman")

pacman::p_load(dplyr, magrittr, rsample, ggplot2)

Sample data

As in previous posts, we’ll use a small sample (download here) of the Lending Club dataset available on Kaggle.

sample <- read.csv("credit_sample.csv")

Creating a target

The next step is to create a target (dependent variable) to model for.

# Mark which loan status will be tagged as default

codes <- c("Charged Off", "Does not meet the credit policy. Status:Charged Off")

# Apply above codes and create target

sample %<>% mutate(bad_flag = ifelse(loan_status %in% codes, 1, 0))

# Replace missing values with a default value

sample[is.na(sample)] <- -1

# Get summary tally

table(sample$bad_flag)

##

## 0 1

## 8838 1162

Sampling

We’ll use bootstrapped sampling to create multiple training sets. We will then repeatedly train a model on each training set and assess the variability in volatile model predictions across score ranges. We’ll use the bootstraps() function in the rsample package.

# Create 100 samples

boot_sample <- bootstraps(data = sample, times = 100)

head(boot_sample, 3)

## # A tibble: 3 × 2

## splits id

## <list> <chr>

## 1 <split [10000/3621]> Bootstrap001

## 2 <split [10000/3617]> Bootstrap002

## 3 <split [10000/3666]> Bootstrap003

boot_sample$splits[[1]]

## <Analysis/Assess/Total>

## <10000/3621/10000>

Each row represents a separate bootstrapped sample whereas within each sample, there are two sub-samples namely an analysis set and an assessment set. To retrieve a bootstrapped sample as a data.frame, the package provides two helper functions - analysis() and assessment()

# Show the first 5 rows and 5 columns of the first sample

analysis(boot_sample$splits[[1]]) %>% .[1:5, 1:5]

## V1 id member_id loan_amnt funded_amnt

## 8823 39052 59271494 -1 15000 15000

## 8907 82937 49197911 -1 12000 12000

## 8384 38625 112870855 -1 10000 10000

## 6579 97794 129904408 -1 29400 29400

## 5579 6494 1368450 -1 1500 1500

The getting started page of the rsample package has additional information.

Creating a modeling function

We’ll use a simple glm() model for illustrative purposes. First, we’ll need to create a function that fits such a model to a given dataset

glm_model <- function(df){

# Fit a simple model with a set specification

mdl <- glm(bad_flag ~

loan_amnt + funded_amnt + annual_inc + delinq_2yrs +

inq_last_6mths + mths_since_last_delinq + fico_range_low +

mths_since_last_record + revol_util + total_pymnt,

family = "binomial",

data = df)

# Return fitted values

return(predict(mdl))

}

# Test the function

# Retrieve a data frame

train <- analysis(boot_sample$splits[[1]])

# Predict

pred <- glm_model(train)

# Check output

range(pred) # Output is on log odds scale

## [1] -19.3723801 0.9013321

Fitting the model repeatedly

Now we need to fit the model repeatedly on each of the bootstrapped samples and store the fitted values. And since we are using R, for-loops are not allowed 😆

# First apply the glm fitting function to each of the sample

# Note the use of lapply

output <- lapply(boot_sample$splits, function(x){

train <- analysis(x)

pred <- glm_model(train)

return(pred)

})

# Collate all predictions into a vector

boot_preds <- do.call(c, output)

range(boot_preds)

## [1] -133.837276 9.449129

# Get outliers

q_high <- quantile(boot_preds, 0.99)

q_low <- quantile(boot_preds, 0.01)

# Truncate the overall distribution to within the lower 1% and upper 1% quantiles

# Doing this since it creates issues later on when scaling the output

boot_preds[boot_preds > q_high] <- q_high

boot_preds[boot_preds < q_low] <- q_low

range(boot_preds)

## [1] -5.0077892 -0.2118255

# Convert to a data frame

boot_preds <- data.frame(pred = boot_preds,

id = rep(1:length(boot_sample$splits), each = nrow(sample)))

head(boot_preds)

## pred id

## 1 -2.6577589 1

## 2 -3.6382487 1

## 3 -0.5991623 1

## 4 -0.4766980 1

## 5 -1.9934515 1

## 6 -2.8314833 1

Scaling model predictions

Given log-odds, we can now scale the output and make it look like a credit score. We’ll use the industry standard points to double odds methodology.

scaling_func <- function(vec, PDO = 30, OddsAtAnchor = 5, Anchor = 700){

beta <- PDO / log(2)

alpha <- Anchor - PDO * OddsAtAnchor

# Simple linear scaling of the log odds

scr <- alpha - beta * vec

# Round off

return(round(scr, 0))

}

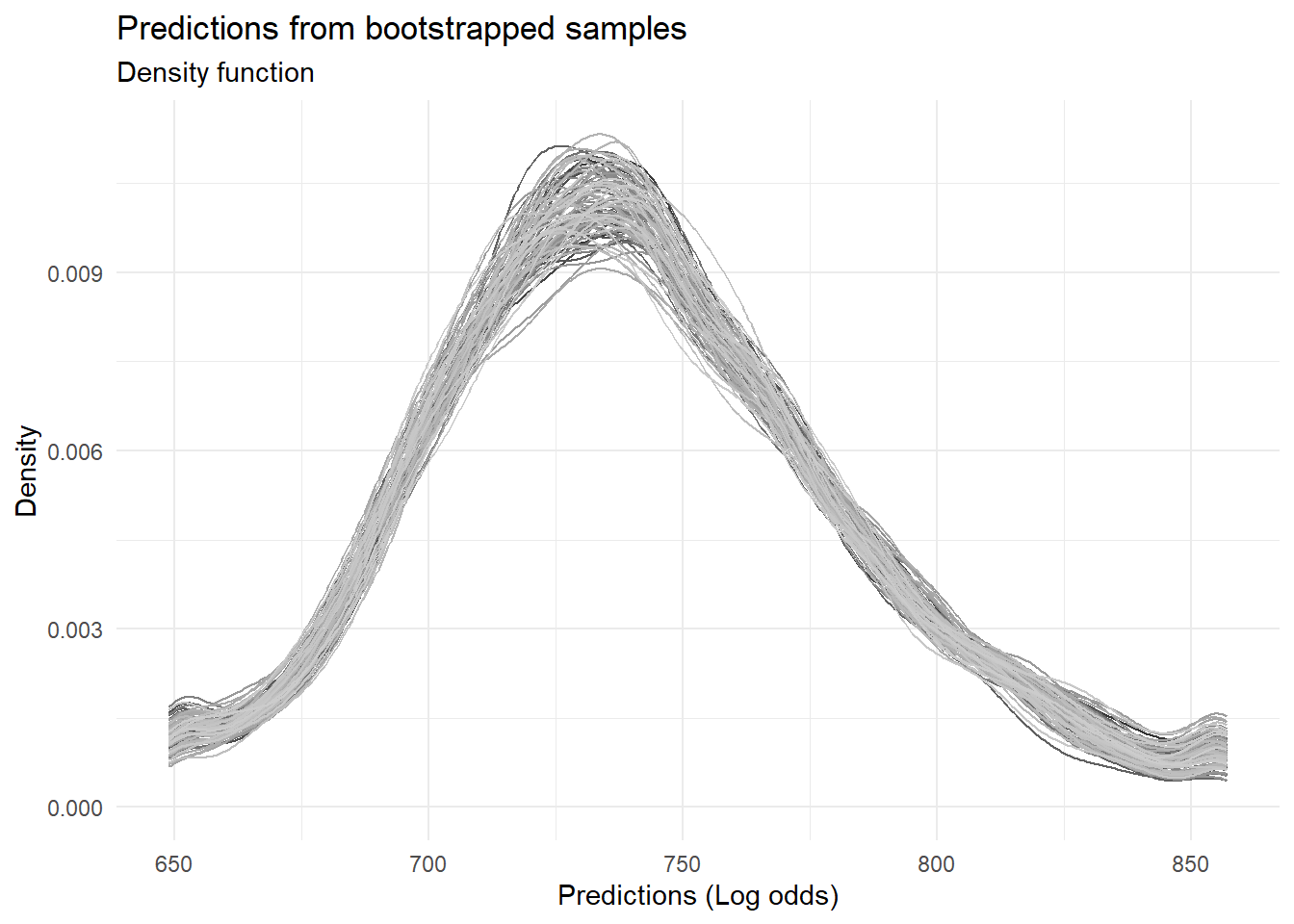

boot_preds$scores <- scaling_func(boot_preds$pred, 30, 2, 700)

# Chart the distribution of predictions across all the samples

ggplot(boot_preds, aes(x = scores, color = factor(id))) +

geom_density() +

theme_minimal() +

theme(legend.position = "none") +

scale_color_grey() +

labs(title = "Predictions from bootstrapped samples",

subtitle = "Density function",

x = "Predictions (Log odds)",

y = "Density")

Assessing variability

Now that we have model predictions for each bootstrapped sample scaled in the form of a score, we can evaluate the variability in these predictions in a visual manner.

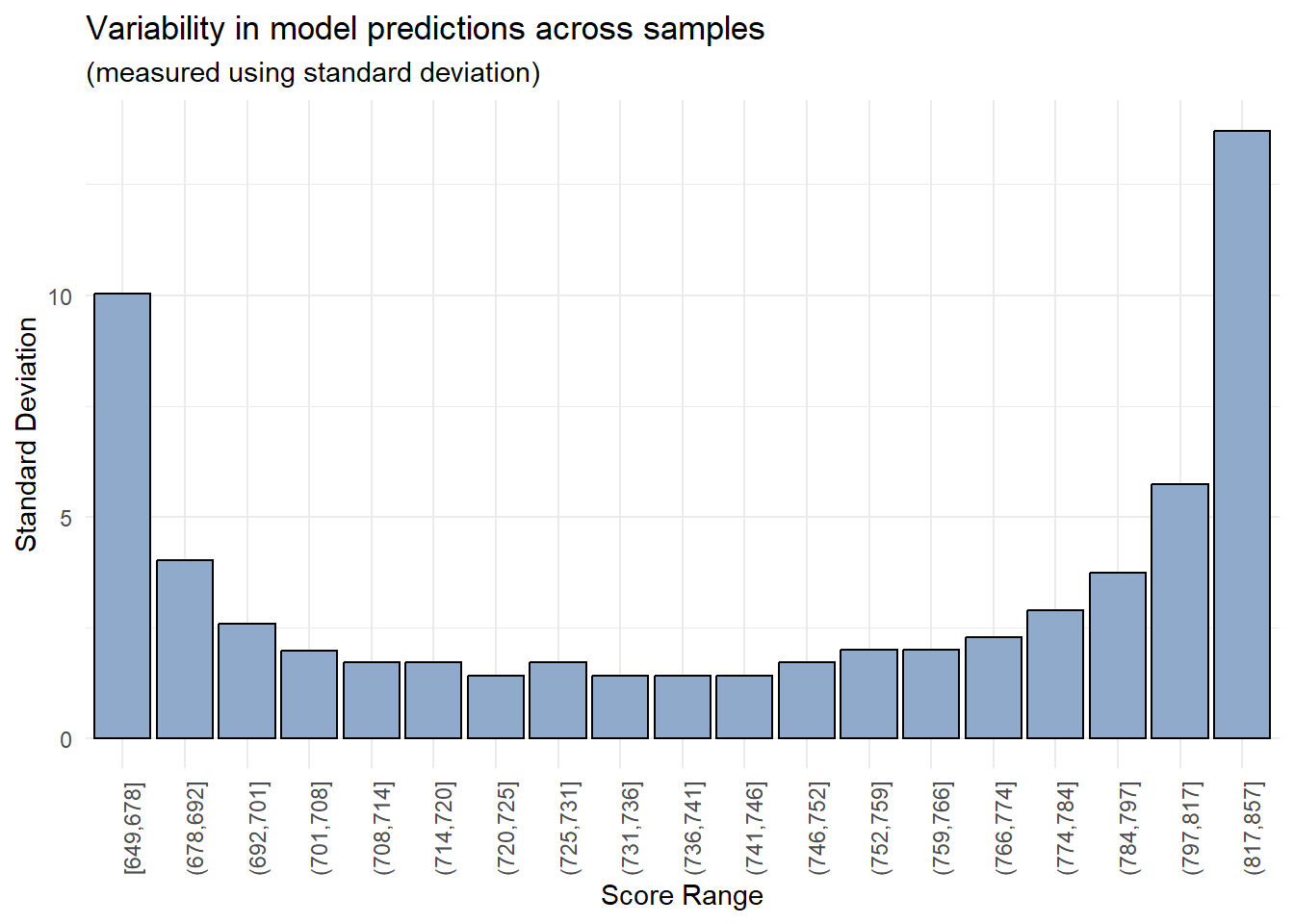

# Create bins using quantiles

breaks <- quantile(boot_preds$scores, probs = seq(0, 1, length.out = 20))

boot_preds$bins <- cut(boot_preds$scores, breaks = unique(breaks), include.lowest = T, right = T)

# Chart standard deviation of model predictions across each score bin

boot_preds %>%

group_by(bins) %>%

summarise(std_dev = sd(scores)) %>%

ggplot(aes(x = bins, y = std_dev)) +

geom_col(color = "black", fill = "#90AACB") +

theme_minimal() +

theme(axis.text.x = element_text(angle = 90)) +

theme(legend.position = "none") +

labs(title = "Variability in model predictions across samples",

subtitle = "(measured using standard deviation)",

x = "Score Range",

y = "Standard Deviation")

As expected, the model’s predictions are more reliable within a certain range of values (700-800) whereas there is significant variability in the model’s predictions in the lowest and highest score buckets.

Parting notes

While the outcome of this experiment is not unexpected, an interesting question could be - should analysts and model users define an operating range for their models? In this example, we could set lower and upper limits at 700 and 800 respectively and any borrower receiving a score beyond these thresholds could be assigned a generic value of 700- or 800+.

That said, binning features mitigates this to a certain extent since the model cannot generate predictions beyond a certain range of values.

An useful extension

Special thanks to Richard Warnung for his comments

In the above analysis, not only did we fit the model repeatedly on different datasets, but we made predictions on different datasets as well. We can remove the effects of the latter if we make predictions on the same test dataset. Here’s some code to do this.

# Create overall training and testing datasets

id <- sample(1:nrow(sample), size = nrow(sample)*0.8, replace = F)

train_data <- sample[id,]

test_data <- sample[-id,]

# Bootstrapped samples are now pulled only from the overall training dataset

boot_sample <- bootstraps(data = train_data, times = 80)

# Using the same function from before but predicting on the same test dataset

glm_model <- function(train, test){

mdl <- glm(bad_flag ~

loan_amnt + funded_amnt + annual_inc + delinq_2yrs +

inq_last_6mths + mths_since_last_delinq + fico_range_low +

mths_since_last_record + revol_util + total_pymnt,

family = "binomial",

data = train)

return(predict(mdl, newdata = test))

}

# Train and predict repeatedly

output <- lapply(boot_sample$splits, function(x){

train <- analysis(x)

pred <- glm_model(train, test_data)

return(pred)

})

# Collate data into a single data.frame

boot_preds <- do.call(c, output)

boot_preds <- data.frame(pred = boot_preds,

id = rep(1:length(boot_sample$splits), each = nrow(sample)))

boot_preds$scores <- scaling_func(boot_preds$pred, 30, 2, 700)

# Forcing scores to a range

boot_preds$scores <- sapply(boot_preds$scores, min, 900)

# Bin the outputs for easier charting

breaks <- quantile(boot_preds$scores, probs = seq(0, 1, length.out = 20))

boot_preds$bins <- cut(boot_preds$scores, breaks = unique(breaks), include.lowest = T, right = T)

# Chart

boot_preds %>%

group_by(bins) %>%

summarise(std_dev = sd(scores)) %>%

ggplot(aes(x = bins, y = std_dev)) +

geom_col(color = "black", fill = "#90AACB") +

theme_minimal() +

theme(axis.text.x = element_text(angle = 90)) +

theme(legend.position = "none") +

labs(title = "Variability in model predictions across samples",

subtitle = "Prediction set is fixed",

x = "Score Range",

y = "Standard Deviation")

Thoughts? Comments? Helpful? Not helpful? Like to see anything else added in here? Let me know!